2026 Social Security COLA: Understanding Your 3.2% Increase

Decoding the 2026 Social Security COLA: What a 3.2% Increase Means for Beneficiaries

For millions of Americans, Social Security benefits represent a cornerstone of their financial security in retirement. Each year, the Social Security Administration (SSA) announces a Cost-of-Living Adjustment (COLA) to ensure that these benefits keep pace with inflation. As we look ahead to 2026, projections suggest a significant Social Security COLA 2026 increase of approximately 3.2%. This adjustment, while not yet final, holds substantial implications for retirees, disabled individuals, and other beneficiaries. Understanding the mechanics behind this increase, its potential impact on your finances, and broader economic considerations is crucial for effective financial planning.

The concept of COLA is rooted in the very purpose of Social Security: to provide a safety net that adapts to economic realities. Without regular adjustments, the purchasing power of benefits would erode over time due to inflation, leaving beneficiaries struggling to cover essential expenses. Therefore, the annual COLA is a vital mechanism designed to preserve the real value of Social Security payments, allowing recipients to maintain a stable standard of living even as prices for goods and services rise.

This article will delve deep into the projected 3.2% Social Security COLA 2026. We will explore how this figure is determined, examine its potential effects on different beneficiary groups, discuss the interplay between COLA and Medicare premiums, and consider the long-term outlook for Social Security. Our aim is to provide a comprehensive, SEO-optimized guide that empowers you with the knowledge to understand and navigate these important changes.

What is the Social Security COLA and How is it Calculated?

The Cost-of-Living Adjustment (COLA) is an annual increase in Social Security and Supplemental Security Income (SSI) benefits. Its primary goal is to offset the effects of inflation, ensuring that the purchasing power of benefits remains relatively constant. Without COLA, the fixed income of retirees and other beneficiaries would steadily decline in real terms, making it increasingly difficult to afford necessities like food, housing, and healthcare.

The Role of the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W)

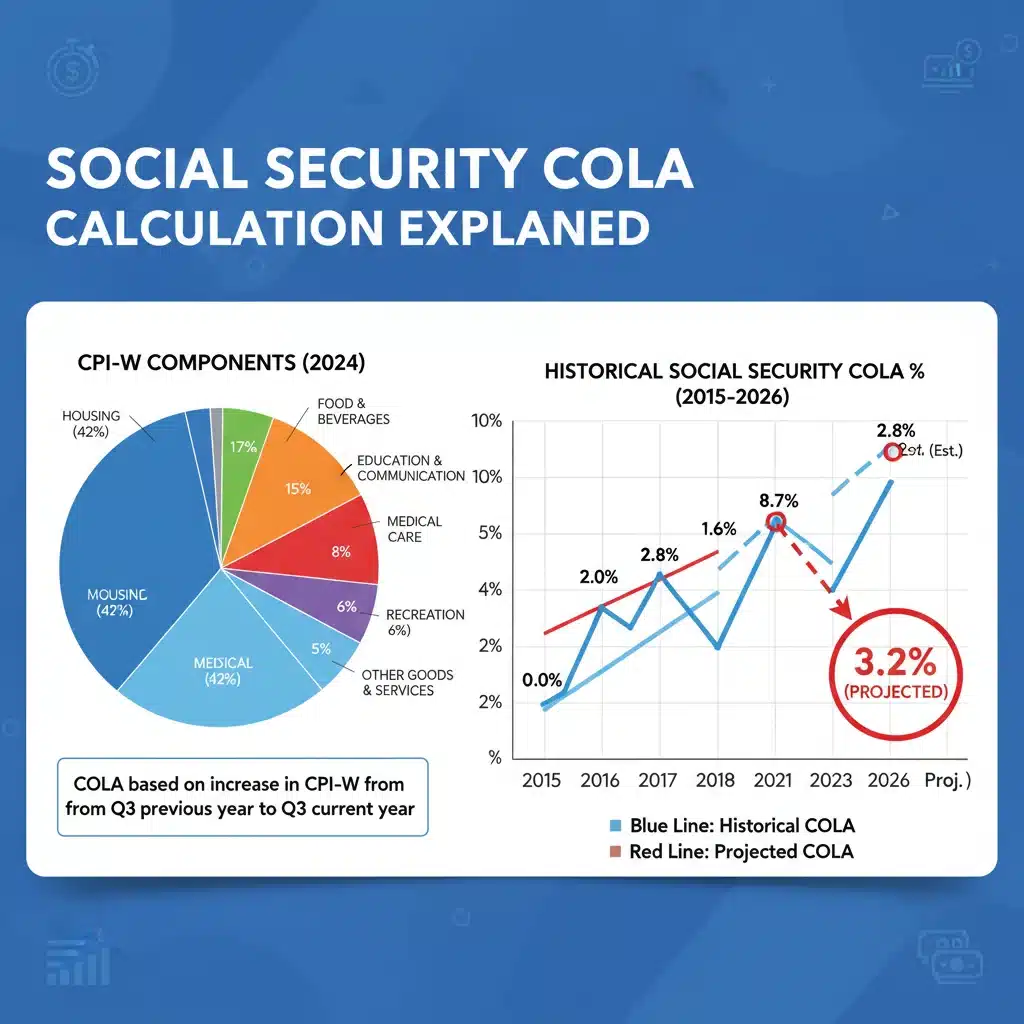

The calculation of the Social Security COLA is not arbitrary; it is directly tied to a specific inflation index: the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index, published by the Bureau of Labor Statistics (BLS), measures the average change over time in the prices paid by urban wage earners and clerical workers for a market basket of consumer goods and services.

Here’s how the calculation generally works:

- Reference Period: The SSA compares the average CPI-W for the third quarter (July, August, and September) of the current year (in this case, 2025) with the average CPI-W for the third quarter of the most recent year in which a COLA was payable.

- Percentage Increase: If there is an increase, the percentage difference between these two averages determines the COLA. For example, if the average CPI-W for Q3 2025 is 3.2% higher than the average CPI-W for Q3 2024 (assuming a COLA was paid in 2025), then the 2026 COLA would be 3.2%.

- No Decrease: Importantly, Social Security benefits can never decrease due to a COLA. If the CPI-W shows no increase or a decrease, the COLA will be zero, and benefits will remain at their current level.

The use of CPI-W has been a subject of debate. Critics argue that CPI-W may not accurately reflect the spending patterns of seniors, who typically spend a larger proportion of their income on healthcare costs compared to urban wage earners. Some advocate for the use of the Consumer Price Index for the Elderly (CPI-E), which specifically tracks the spending habits of those aged 62 and older. However, current legislation mandates the use of CPI-W.

Why the 3.2% Projection for 2026?

The 3.2% projection for the Social Security COLA 2026 is based on current economic forecasts and inflation trends. These projections are often made by various organizations, including the Social Security Administration’s actuaries, the Congressional Budget Office (CBO), and independent economic research firms. They analyze factors such as:

- Current Inflation Rates: Persistent inflation in key sectors like housing, energy, and food contributes significantly to rising CPI-W figures.

- Economic Growth: A robust economy can sometimes lead to higher demand and, consequently, higher prices.

- Global Events: Geopolitical events, supply chain disruptions, and global energy market fluctuations can all impact domestic inflation.

- Federal Reserve Policy: Interest rate changes and other monetary policies by the Federal Reserve influence inflation expectations.

It’s crucial to remember that this 3.2% is a projection. The final COLA will only be announced in October 2025, after the CPI-W data for July, August, and September 2025 is fully compiled and analyzed. However, these early projections provide valuable insight for beneficiaries to begin planning.

Impact of a 3.2% COLA on Your Social Security Benefits

A 3.2% increase in the Social Security COLA 2026 could translate into a noticeable difference in monthly benefit checks for millions of Americans. While the percentage might seem small, its cumulative effect over a year can be significant, especially for those who rely heavily on Social Security as their primary income source.

How Your Monthly Check Could Change

To understand the direct impact, let’s consider an example. If the average monthly Social Security benefit for retired workers in late 2025 is projected to be, say, $1,900, a 3.2% COLA would add approximately $60.80 to that check, bringing it to $1,960.80. Over a year, this would mean an additional $729.60. For couples receiving benefits, the increase would be proportionally higher. These additional funds can help beneficiaries keep pace with rising costs of living, from groceries to utility bills.

It’s important to note that the actual dollar amount of your increase will depend on your specific benefit amount. Individuals receiving higher benefits will see a larger dollar increase, while those with lower benefits will see a smaller, though still impactful, adjustment.

Medicare Premiums and the ‘Hold Harmless’ Provision

One of the most critical factors to consider when discussing COLA is its interaction with Medicare Part B premiums. For many beneficiaries, Medicare Part B premiums are deducted directly from their Social Security checks. This is where the ‘hold harmless’ provision comes into play.

The ‘hold harmless’ provision prevents a beneficiary’s net Social Security payment from decreasing due to an increase in Medicare Part B premiums. This means that if your Medicare Part B premium increase is greater than your COLA increase, your premium will be adjusted so that your monthly Social Security benefit does not go down. This protection primarily applies to beneficiaries who have their Part B premiums deducted from their Social Security checks and whose premiums are not already being paid by Medicaid or a third party.

However, the ‘hold harmless’ provision does not apply to all beneficiaries:

- New Medicare enrollees.

- Beneficiaries who pay their Part B premiums directly (not deducted from Social Security).

- High-income beneficiaries who pay an Income-Related Monthly Adjustment Amount (IRMAA) for Part B and Part D.

For those not covered by ‘hold harmless,’ an increase in Medicare Part B premiums could potentially offset some or all of their Social Security COLA 2026 increase, leading to a smaller net gain or even a slight reduction in their net disposable income, depending on the severity of the premium hike.

Impact on Other Programs and Taxes

A COLA increase can also have ripple effects on other aspects of a beneficiary’s financial life:

- Income Taxes: A higher Social Security benefit could push some beneficiaries into a higher tax bracket or cause a larger portion of their benefits to become taxable. The taxation of Social Security benefits depends on your ‘combined income,’ which includes your adjusted gross income, tax-exempt interest, and half of your Social Security benefits.

- SSI Benefits: Supplemental Security Income (SSI) benefits also receive a COLA, typically mirroring the Social Security COLA. This is crucial for low-income individuals and families.

- Means-Tested Programs: For beneficiaries receiving assistance from other means-tested government programs, a higher Social Security benefit could potentially affect their eligibility or the level of benefits they receive from those programs. It’s essential to understand the income thresholds for any additional aid you might be receiving.

Navigating these interactions requires careful consideration and, in some cases, professional financial advice. Understanding how COLA impacts your overall financial picture is key to effective retirement planning.

Broader Economic Implications of the 2026 COLA

The Social Security COLA 2026 is not just about individual benefit checks; it also has broader implications for the economy and the solvency of the Social Security program itself. A significant COLA reflects underlying economic conditions and can influence consumer spending, inflation expectations, and government fiscal policy.

COLA and Inflationary Environment

A 3.2% COLA suggests that inflation is expected to remain a relevant factor in the economy leading up to 2026. While not as high as some of the COLAs seen in recent years (e.g., 5.9% for 2022, 8.7% for 2023), it still indicates that the purchasing power of money is being eroded. For beneficiaries, this COLA is a necessary adjustment to help mitigate that erosion.

However, the relationship is cyclical: higher inflation leads to higher COLAs, which in turn inject more money into the economy, potentially fueling further inflation. Policymakers constantly monitor this dynamic to ensure economic stability without undermining the financial well-being of seniors.

Impact on Consumer Spending and the Economy

Social Security benefits represent a substantial portion of consumer spending, particularly among older demographics. A higher COLA means more disposable income for millions of people, which can translate into increased spending on goods and services. This boost in consumer demand can stimulate economic activity, supporting businesses and jobs.

However, the impact varies. For beneficiaries who struggle to make ends meet, the increased funds will likely go towards essential expenses, providing critical relief. For those with more discretionary income, it might lead to increased spending on leisure, travel, or other non-essential items, contributing to broader economic growth.

Social Security Trust Fund Solvency

The long-term solvency of the Social Security program is a perennial concern. Each COLA increase, while necessary for beneficiaries, also means a larger outflow of funds from the Social Security trust funds. This adds to the ongoing debate about how to ensure the program’s financial health for future generations.

Factors influencing solvency include:

- Demographics: An aging population and lower birth rates mean fewer workers contributing to the system relative to the number of retirees receiving benefits.

- Wage Growth: Slower wage growth can limit the amount of payroll taxes collected.

- Investment Returns: The trust funds invest in special U.S. Treasury securities, and their returns also play a role.

While a 3.2% COLA is a standard adjustment, the cumulative effect of annual COLAs, especially during periods of higher inflation, naturally puts pressure on the trust funds. This often reignites discussions about potential policy changes, such as adjusting the full retirement age, modifying the COLA calculation method, or increasing payroll taxes.

Preparing for the 2026 Social Security COLA: Financial Planning Tips

Understanding the projected Social Security COLA 2026 is the first step; the next is to incorporate this information into your personal financial planning. Even a modest increase can, when combined with other financial decisions, significantly impact your retirement security.

Review Your Budget and Expenses

With a projected 3.2% increase, now is an excellent time to review your current budget. How do your expenses compare to your income? Are there areas where costs have increased more than the COLA? Identifying these areas can help you allocate your increased benefits effectively. Pay close attention to rising costs in healthcare, housing, and food, as these are often the largest expenditures for retirees.

- Track Spending: Use budgeting apps or spreadsheets to get a clear picture of where your money goes.

- Identify Inflation Hotspots: Note which categories of your spending have seen the most significant price increases.

- Adjust Allocations: Reallocate funds to cover these higher costs, ensuring your essential needs are met.

Consider the Impact of Medicare Part B Premiums

As discussed, Medicare Part B premiums can significantly affect your net Social Security benefit. While the ‘hold harmless’ provision offers protection for many, it’s not universal. Stay informed about the projected Medicare Part B premium increases for 2026, which are typically announced around the same time as the COLA. Factor these potential premium hikes into your budget to avoid any surprises.

If you are a high-income earner, be aware that your IRMAA surcharges could also increase, further impacting your net benefit. Consulting with a financial advisor or Medicare specialist can help you understand your specific situation.

Tax Planning for Increased Benefits

A higher Social Security benefit, combined with other retirement income (pensions, 401(k) withdrawals, investment gains), could potentially lead to a larger portion of your Social Security benefits being subject to federal income tax. Depending on your ‘combined income,’ up to 85% of your Social Security benefits may be taxable.

Consider the following proactive steps:

- Estimate Taxable Income: Work with a tax professional to estimate your total taxable income for 2026, including the increased Social Security benefits.

- Adjust Withholding: If necessary, adjust your income tax withholding or make estimated tax payments to avoid a large tax bill or penalties at the end of the year.

- Roth Conversions: For some, strategic Roth IRA conversions might be a way to manage future taxable income, though this is a complex strategy that requires careful planning.

Long-Term Financial Security

While the Social Security COLA 2026 provides a welcome boost, it’s crucial to view it within the context of your broader long-term financial security. Don’t rely solely on COLA to meet all your financial needs. Continue to:

- Diversify Income Streams: If possible, explore ways to supplement your Social Security benefits with other income sources, such as part-time work, annuities, or investment income.

- Manage Debt: Reducing or eliminating high-interest debt can free up more of your COLA increase for essential spending or savings.

- Review Investment Portfolio: Ensure your investment portfolio aligns with your risk tolerance and financial goals, especially in an inflationary environment.

- Estate Planning: Regularly review your estate plan to ensure it reflects your current wishes and financial situation.

By taking a proactive approach, beneficiaries can maximize the positive impact of the Social Security COLA 2026 and strengthen their overall financial resilience.

Looking Ahead: The Future of Social Security and COLA

The projected 3.2% Social Security COLA 2026 is a snapshot in time, reflecting current economic conditions. However, the future of Social Security and its annual adjustments is subject to ongoing economic, demographic, and political considerations.

Forecasting Future COLAs

Forecasting future COLAs involves a degree of uncertainty. While economists can make educated guesses based on current trends, unexpected events (e.g., global recessions, pandemics, significant supply chain disruptions) can dramatically alter inflation rates. Therefore, it’s wise for beneficiaries to approach future COLA projections with a degree of flexibility in their financial planning.

Long-term projections for inflation vary, which means future COLAs could fluctuate. Some analysts anticipate a return to lower, more stable inflation rates, which would lead to smaller COLA increases. Others worry about persistent inflationary pressures, which would necessitate larger adjustments to maintain purchasing power.

Potential Reforms to Social Security

Discussions about Social Security reform are continuous, driven by concerns over the program’s long-term solvency. While a 3.2% COLA helps beneficiaries today, the underlying financial challenges remain. Potential reforms often include:

- Changes to COLA Calculation: proposals to switch from CPI-W to CPI-E (which could result in slightly higher COLAs, though not guaranteed) or to a chained CPI (which typically yields lower COLAs).

- Adjusting the Full Retirement Age: Gradually increasing the age at which individuals can claim their full benefits.

- Increasing Payroll Taxes: Raising the Social Security tax rate or increasing the cap on earnings subject to Social Security taxes.

- Means-Testing Benefits: Reducing benefits for high-income retirees.

Any significant reform would require legislative action and would likely be a complex and contentious process. Beneficiaries should stay informed about these debates, as they could have a profound impact on future benefits.

The Importance of Personal Savings

Regardless of future COLA adjustments or potential reforms, the importance of personal savings and diversified retirement income streams cannot be overstated. Social Security was always intended to be a foundational layer of retirement income, not the sole source.

By diligently saving throughout your working life, investing wisely, and exploring other retirement income options (e.g., 401(k)s, IRAs, pensions, personal investments), you can build a more robust financial future that is less susceptible to the uncertainties of COLA projections or changes in Social Security policy. Even a 3.2% increase, while helpful, may not cover all rising costs, underscoring the need for a multi-faceted approach to retirement planning.

Conclusion

The anticipated 3.2% Social Security COLA 2026 offers a welcome adjustment for millions of beneficiaries, helping to preserve the purchasing power of their hard-earned benefits in the face of ongoing inflation. This increase, tied directly to the CPI-W, reflects the economic realities of rising costs for everyday goods and services.

While the final figure will be confirmed in October 2025, the projection provides a valuable opportunity for proactive financial planning. Beneficiaries should consider how this increase will affect their monthly budget, the interaction with Medicare Part B premiums, and potential tax implications. Reviewing your overall financial strategy, including other income sources and expenses, is crucial to maximize the benefit of this COLA.

Looking ahead, the landscape of Social Security is dynamic, influenced by economic trends, demographic shifts, and ongoing policy discussions. Staying informed about these developments and maintaining a diversified approach to retirement savings will empower you to navigate the future with greater confidence and security. The Social Security COLA 2026 is more than just a number; it’s a vital component of financial well-being for millions of Americans, deserving of careful attention and informed planning.