Maximizing Your 401(k) Contributions in 2026: Understanding the $23,000 Limit Increase

As we look towards 2026, many individuals are already strategizing their financial futures, and a key component of that planning revolves around retirement savings. Specifically, understanding and leveraging the changes to 401k contribution limits is paramount. The Internal Revenue Service (IRS) periodically adjusts these limits to account for inflation and other economic factors, and for 2026, the anticipated increase to $23,000 for elective deferrals into 401(k), 403(b), and 457 plans presents a significant opportunity for savers. This comprehensive guide will delve into the nuances of these changes, offering actionable strategies to help you maximize your retirement savings and secure your financial future.

The 401(k) plan remains one of the most powerful tools for retirement savings available to employees. Its tax-advantaged nature, coupled with potential employer matching contributions, makes it an indispensable asset in any long-term financial strategy. Failing to utilize this vehicle to its fullest potential can mean leaving significant money on the table, both in terms of tax savings and compounded growth. Therefore, staying informed about the latest 401k contribution limits and how to effectively navigate them is crucial.

Understanding the 2026 401(k) Contribution Limits

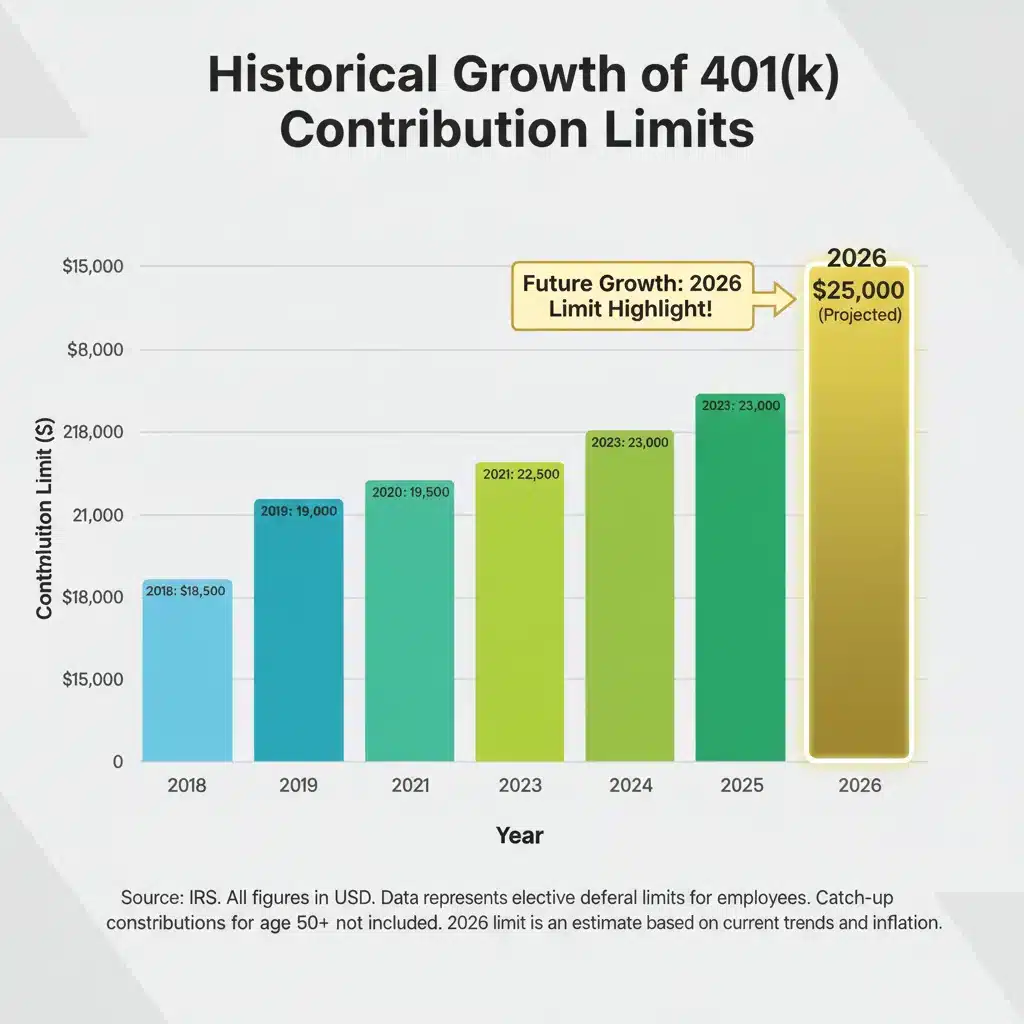

The projected increase of the standard 401(k) contribution limit to $23,000 for 2026 marks another step in the IRS’s efforts to help Americans save more for retirement. This is a crucial piece of information for anyone planning their financial future. The limit applies to the amount you can contribute from your paycheck on a pre-tax or Roth basis. It’s important to distinguish this from the total amount that can be contributed to your 401(k) account, which includes employer contributions and other additions. We’ll explore the overall limit later, but for now, let’s focus on your personal elective deferral.

This $23,000 limit represents a significant opportunity. For individuals who have consistently contributed the maximum in previous years, this increase allows them to set aside an additional sum, further accelerating their retirement savings. For those just starting or looking to ramp up their contributions, it serves as an ambitious yet attainable goal. The power of compounding interest means that every dollar contributed earlier and in larger amounts can lead to substantially greater wealth accumulation over time. Understanding these 401k contribution limits is the first step towards optimizing your retirement strategy.

It’s also worth noting that these limits are often adjusted annually based on inflation. While the $23,000 figure is a strong projection for 2026, it’s always wise to confirm the official IRS announcements as they become available. However, planning based on this projected increase allows you to prepare financially and adjust your budget accordingly.

The Power of Catch-Up Contributions for Older Savers

For individuals aged 50 and over, the IRS provides an additional benefit designed to help them make up for lost time or simply supercharge their savings as they approach retirement. These are known as catch-up contributions. While the exact catch-up limit for 2026 has not been officially released, based on historical trends and inflation adjustments, it is also expected to see an increase. In recent years, this limit has been around $7,500, allowing those eligible to contribute significantly more than the standard limit.

If you are 50 or older, you can contribute the standard $23,000 plus the catch-up amount, potentially allowing you to put away over $30,000 into your 401(k) in 2026. This is an incredibly powerful tool for retirement planning, especially for those who may have started saving later in life or experienced periods where they couldn’t contribute as much. Maximizing both the standard and catch-up 401k contribution limits can dramatically alter your retirement outlook.

Consider the impact of these additional contributions. An extra $7,500 per year, compounded over 10-15 years, can translate into hundreds of thousands of dollars more in your retirement nest egg. This is not just about having more money; it’s about having more security, more flexibility, and potentially an earlier retirement date. Don’t overlook this crucial provision if you qualify.

Employer Matching Contributions: Don’t Leave Money on the Table

One of the most attractive features of a 401(k) plan is the potential for employer matching contributions. Many companies offer to match a certain percentage of their employees’ contributions, often up to a specific limit. This is essentially free money, and failing to contribute at least enough to receive the full employer match is one of the biggest financial mistakes an employee can make.

For instance, if your employer matches 50 cents on the dollar up to 6% of your salary, and you earn $100,000, contributing $6,000 of your own money would net you an additional $3,000 from your employer. This effectively gives you an immediate 50% return on that portion of your investment, a return that is virtually impossible to achieve elsewhere. When considering the 401k contribution limits, always prioritize contributing enough to capture the full employer match first.

Even if you cannot reach the full $23,000 individual limit, ensuring you get the maximum employer match should be your primary goal. This strategy significantly boosts your retirement savings with minimal effort on your part, leveraging a benefit that is often a core part of your compensation package. Review your plan documents or speak with your HR department to understand your employer’s matching policy and make sure you’re taking full advantage.

Total 401(k) Contribution Limit: Beyond Your Deferrals

While the $23,000 limit (and potential catch-up contributions) refers to your elective deferrals, there’s a higher overall limit for total contributions to a 401(k) plan. This total limit includes your contributions, your employer’s matching contributions, and any profit-sharing contributions. For 2026, this overall limit is also expected to increase, potentially reaching around $69,000, or even higher for those eligible for catch-up contributions.

Understanding this total limit is crucial, especially for high-income earners or those with generous employers. While most individuals will focus on maximizing their personal elective deferrals, it’s good to be aware of the bigger picture. If your employer offers substantial contributions, it might be possible to reach this higher overall limit. This is particularly relevant for small business owners who might contribute to their own 401(k) as both employee and employer.

This higher limit underscores the significant tax advantages of a 401(k). Contributions grow tax-deferred, meaning you don’t pay taxes on the investment gains until you withdraw the money in retirement. This long-term deferral allows your investments to compound more aggressively, leading to a larger nest egg. Keeping an eye on all aspects of 401k contribution limits, including the total limit, provides a holistic view for advanced financial planning.

Strategies for Maximizing Your 401(k) Contributions

Reaching the maximum 401k contribution limits can seem daunting, especially if you’re not used to saving aggressively. However, with a few strategic approaches, it’s an achievable goal for many. Here are some effective strategies:

1. Automate Your Contributions

The simplest and most effective way to ensure you’re contributing consistently is to automate your payroll deductions. Set up your contributions to be deducted directly from each paycheck. This ‘set it and forget it’ approach ensures you’re consistently saving without having to actively think about it each pay period. If you aim for the $23,000 limit, divide that by the number of paychecks you receive in a year (e.g., 24 for bi-weekly, 26 for semi-monthly) to determine your per-paycheck contribution amount.

2. Increase Contributions with Raises and Bonuses

Whenever you receive a raise or a bonus, consider allocating a significant portion, if not all, of that extra income towards your 401(k). This strategy allows you to increase your savings without feeling a pinch in your take-home pay, as you’re adjusting your contributions from new money rather than existing expenses. This is a pain-free way to incrementally reach the 401k contribution limits.

3. Review and Adjust Annually

Don’t just set your contribution rate once and forget it for years. Make it a habit to review your 401(k) contributions annually, especially when new limits are announced. This ensures you’re always on track to maximize your savings and take advantage of any increases in the 401k contribution limits. It’s also a good time to re-evaluate your investment allocations within the plan.

4. Understand Your Budget and Cut Expenses

If you’re struggling to find the funds to maximize your 401(k), take a hard look at your budget. Identify areas where you can cut unnecessary expenses. Even small savings, like reducing daily coffee runs or dining out less frequently, can add up over time and free up funds for your retirement account. Every dollar saved and invested early has significant long-term potential.

5. Consider a Roth 401(k) Option

Many employers now offer a Roth 401(k) option. With a Roth 401(k), your contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. This can be particularly advantageous if you anticipate being in a higher tax bracket in retirement than you are now. The same 401k contribution limits apply to both traditional and Roth 401(k)s, allowing you to choose the tax treatment that best suits your financial plan.

The Long-Term Benefits of Maximizing Your 401(k)

The benefits of consistently maximizing your 401k contribution limits extend far beyond simply having a larger sum of money in retirement. They encompass tax advantages, financial security, and peace of mind.

Tax Advantages

For traditional 401(k)s, your contributions are tax-deductible in the year they are made, reducing your current taxable income. This means you pay less in taxes today. The money then grows tax-deferred until retirement. For Roth 401(k)s, while contributions are after-tax, qualified withdrawals in retirement are completely tax-free. Both options offer significant tax benefits that can lead to substantial savings over decades.

Compounding Growth

The magic of compounding interest is perhaps the most powerful aspect of long-term investing. When your investments earn returns, those returns then earn their own returns, leading to exponential growth over time. By maximizing your 401k contribution limits early and consistently, you give your money more time and more capital to compound, resulting in a much larger retirement nest egg.

Financial Security and Flexibility

A robust 401(k) balance provides unparalleled financial security in retirement. It means you’ll be less reliant on Social Security and more in control of your financial destiny. A larger nest egg also offers greater flexibility – whether you want to retire earlier, pursue new passions, or simply enjoy a comfortable lifestyle without financial worries. Maximizing your contributions is a direct path to this security.

What Happens If You Can’t Max Out Your 401(k)?

While the goal is often to hit the maximum 401k contribution limits, it’s important to be realistic about your personal financial situation. Not everyone can afford to contribute the full $23,000 (or more) each year, and that’s perfectly okay. The most important thing is to contribute what you can consistently.

If you can’t max out your 401(k), here’s what you should prioritize:

- Get the Employer Match: As mentioned, this is free money. Always contribute at least enough to get the full employer match.

- Contribute What You Can Afford: Even small, consistent contributions add up significantly over time thanks to compounding. Don’t let the perfect be the enemy of the good.

- Increase Gradually: Aim to increase your contribution rate by 1% or 2% each year, or whenever you get a raise. These small increases are often barely noticeable in your paycheck but can make a big difference over decades.

- Consider Other Retirement Accounts: If your 401(k) options are limited or you’ve hit your comfortable contribution level, explore other tax-advantaged accounts like an Individual Retirement Account (IRA) or Roth IRA. These offer additional avenues for retirement savings.

The journey to retirement savings is a marathon, not a sprint. Consistency and incremental progress are often more effective than sporadic, large contributions. Focus on what you can control and build healthy saving habits.

The Role of Investment Choices Within Your 401(k)

While maximizing your 401k contribution limits is critical, the investments you choose within your 401(k) plan are equally important. Your contribution amounts determine how much capital you’re putting to work, but your investment choices determine how effectively that capital grows.

Most 401(k) plans offer a selection of mutual funds, exchange-traded funds (ETFs), or target-date funds. Here are some considerations:

- Diversification: Ensure your portfolio is well-diversified across different asset classes (stocks, bonds, real estate, etc.) to mitigate risk.

- Risk Tolerance: Your investment choices should align with your personal risk tolerance and time horizon. Younger investors with a longer time horizon can typically afford to take on more risk (e.g., higher allocation to stocks), while those closer to retirement may opt for a more conservative approach.

- Fees: Pay attention to the expense ratios of the funds you choose. High fees can eat into your returns over time. Opt for low-cost index funds or ETFs when available.

- Target-Date Funds: These funds offer a convenient, ‘set-it-and-forget-it’ option. They automatically adjust their asset allocation to become more conservative as you approach your target retirement date.

- Rebalancing: Periodically review and rebalance your portfolio to ensure it stays aligned with your desired asset allocation.

Even with optimal 401k contribution limits, poor investment choices can hinder your retirement growth. Take the time to understand the investment options available in your plan and make informed decisions, or seek advice from a qualified financial advisor.

Navigating Potential Future Changes and Economic Factors

While we’re focusing on the 2026 401k contribution limits, it’s important to remember that these limits are subject to annual review and adjustment by the IRS. Economic factors, such as inflation, play a significant role in these adjustments. Staying informed about these potential future changes is part of a proactive retirement planning strategy.

Beyond contribution limits, other elements of retirement planning can also evolve. Tax laws, Social Security regulations, and healthcare costs are all dynamic factors that can impact your retirement. Therefore, a flexible and adaptable financial plan is essential. Regularly reviewing your overall financial strategy, not just your 401(k), will ensure you’re well-prepared for any shifts.

For example, understanding the inflation rate’s impact on your future purchasing power is vital. While $23,000 contributed today is significant, its real value in 20 or 30 years will be different. This is why aggressive saving and wise investing are so crucial – to outpace inflation and maintain your desired lifestyle in retirement. The announced 401k contribution limits are a benchmark, but your overall financial literacy and consistent action are what truly drive success.

Conclusion: Take Action on Your 2026 401(k) Contributions Now

The projected 2026 401k contribution limits, particularly the $23,000 for elective deferrals, offer a fantastic opportunity to boost your retirement savings. Whether you’re a seasoned investor or just beginning your retirement journey, understanding these limits and implementing smart strategies is key to building a secure financial future.

Start by reviewing your current contribution rate. Can you increase it to meet or get closer to the new $23,000 limit? If you’re 50 or over, are you taking full advantage of catch-up contributions? Are you maximizing your employer match? These are critical questions to ask yourself now, well in advance of 2026.

Retirement planning is not a one-time event; it’s an ongoing process that requires attention and adaptation. By staying informed about changes in 401k contribution limits, consistently contributing, and making wise investment choices, you are taking powerful steps towards achieving the retirement you envision. Don’t wait – start planning and adjusting your contributions today to fully leverage the opportunities that 2026 will bring.

for 2025: Limits, Benefits, and Strategy")

2026: Hit the $23,000 Limit & Reduce Taxes")