Student Loan Forgiveness 2026: Policy Shifts & Borrower Impact

The landscape of student loan debt in the United States is continuously evolving, with significant policy shifts and discussions surrounding student loan forgiveness taking center stage. As we look towards 2026, millions of borrowers are eagerly anticipating clarity on what relief programs will be available, how they might qualify, and the broader economic impact of these initiatives. The concept of student loan forgiveness 2026 is not just a distant possibility but a crucial aspect of financial planning for many.

For over 40 million Americans burdened by student debt, the stakes are incredibly high. The ability to manage or even eliminate this debt can profoundly impact individual financial stability, housing decisions, career paths, and overall economic participation. This comprehensive article aims to dissect the current state of student loan forgiveness, project potential scenarios for 2026, and provide actionable insights for borrowers navigating this complex terrain.

Understanding the Current Student Loan Forgiveness Landscape

Before delving into what 2026 might hold, it’s essential to understand the foundation of existing student loan forgiveness programs and the recent changes that have shaped the current environment. The discussion around student loan forgiveness 2026 is built upon years of policy debates, legislative actions, and executive orders.

Before delving into what 2026 might hold, it’s essential to understand the foundation of existing student loan forgiveness programs and the recent changes that have shaped the current environment. The discussion around student loan forgiveness 2026 is built upon years of policy debates, legislative actions, and executive orders.

Historical Context: A Brief Overview of Forgiveness Initiatives

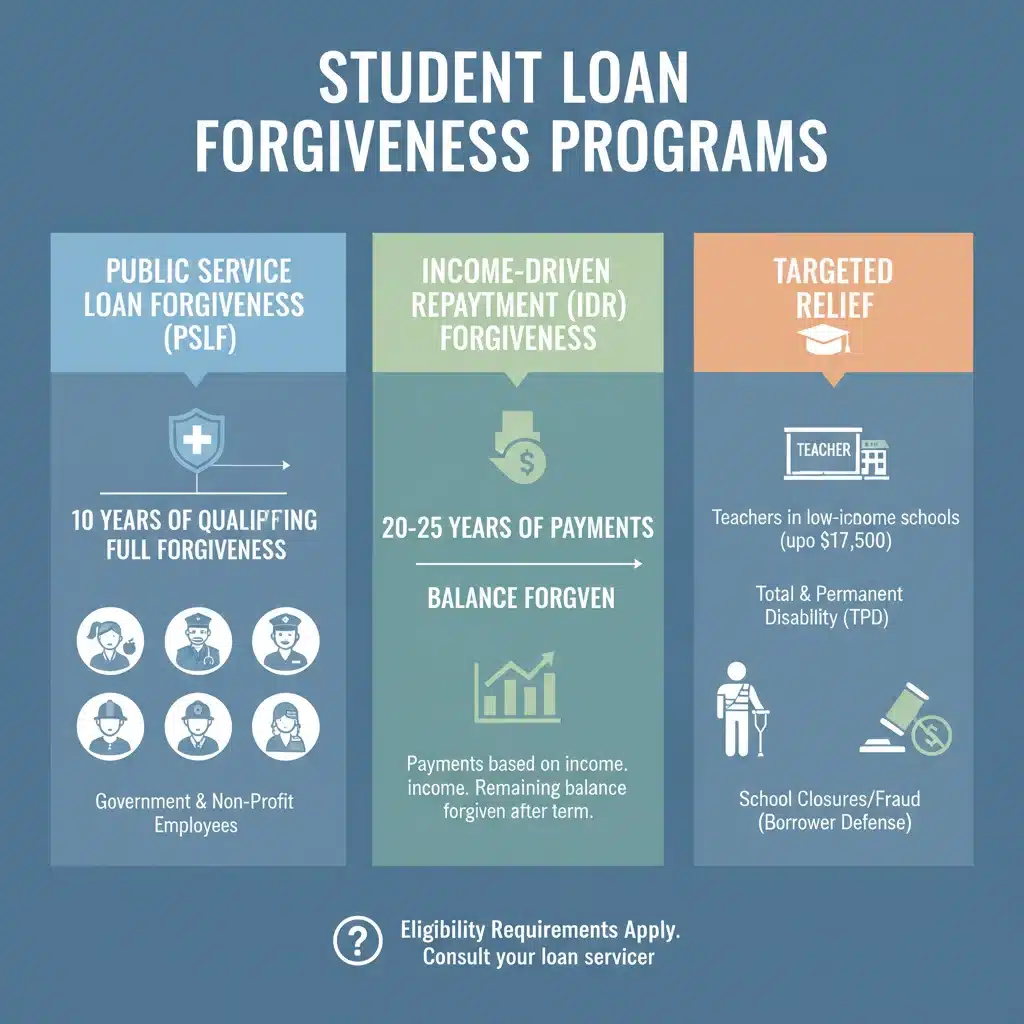

Student loan forgiveness is not a new concept. Several programs have been in place for years, designed to offer relief to specific groups of borrowers. These include:

- Public Service Loan Forgiveness (PSLF): This program forgives the remaining balance on Direct Loans after 120 qualifying monthly payments have been made under a qualifying repayment plan while working full-time for a qualifying employer.

- Income-Driven Repayment (IDR) Plans: These plans cap monthly payments based on income and family size. After 20 or 25 years of payments (depending on the plan and loan type), any remaining balance is forgiven.

- Teacher Loan Forgiveness: Designed for teachers who work for five complete and consecutive academic years in a low-income school or educational service agency.

- Perkins Loan Cancellation: Offered to borrowers in certain professions, such as teaching, nursing, or law enforcement.

- Total and Permanent Disability (TPD) Discharge: For borrowers who are unable to engage in any substantial gainful activity due to a physical or mental impairment.

- Closed School Discharge: For students whose school closed while they were enrolled or shortly after they withdrew.

While these programs have provided relief to many, their complexities, strict eligibility requirements, and often confusing application processes have led to significant challenges and low approval rates in the past. This historical context is crucial for understanding the impetus behind more recent, broader forgiveness efforts and the ongoing conversations about student loan forgiveness 2026.

Recent Policy Shifts and Their Impact

The past few years have seen unprecedented changes in student loan policy, largely driven by the economic fallout of the COVID-19 pandemic and a renewed focus on addressing the student debt crisis. Key developments include:

- The Payment Pause and Interest Freeze: Initiated in March 2020, this federal action paused payments and set interest rates at 0% for most federal student loans. While not forgiveness, it provided significant financial breathing room for millions of borrowers. This pause significantly influenced the discussions leading up to potential student loan forgiveness 2026 strategies.

- Targeted Forgiveness Initiatives: The Biden administration has used executive authority to expand existing forgiveness programs and implement targeted relief. This includes significant changes to PSLF, making it easier for public servants to qualify, and adjustments to IDR plans that have led to billions in forgiven debt for long-term borrowers. These changes have retroactively corrected administrative errors and expanded eligibility for many.

- Proposed Broader Forgiveness Plans: While some broader plans for widespread loan forgiveness faced legal challenges and were ultimately blocked, the political will and public demand for such measures remain strong. These proposals often aimed to provide a set amount of forgiveness (e.g., $10,000 or $20,000) to a large segment of borrowers, with income caps to target relief. The ongoing debate about this kind of comprehensive relief will undoubtedly shape the narrative around student loan forgiveness 2026.

- SAVE Plan (Saving on a Valuable Education): This new income-driven repayment plan, which began implementation in 2023, is designed to significantly reduce monthly payments for many borrowers, particularly those with lower incomes. It also offers a shorter path to forgiveness for some, with balances forgiven after 10 years of payments for those who originally borrowed $12,000 or less. The SAVE plan is a major component of the current administration’s strategy to make student loan repayment more manageable and accessible, potentially reducing the need for future widespread forgiveness but also providing a direct path for many to reach forgiveness by 2026 and beyond.

These policy shifts demonstrate a clear trend towards making student loan repayment more equitable and providing more accessible pathways to forgiveness. Borrowers looking ahead to student loan forgiveness 2026 should pay close attention to the continued evolution of these programs.

Projecting Student Loan Forgiveness in 2026

Predicting the exact state of student loan forgiveness in 2026 requires considering various factors, including the political climate, economic conditions, and ongoing legal challenges. However, based on current trends and discussions, several scenarios are plausible.

Scenario 1: Continued Expansion of Existing Programs

One likely scenario for student loan forgiveness 2026 is the continued expansion and refinement of existing forgiveness programs, particularly PSLF and IDR plans (like the SAVE plan). The current administration has demonstrated a commitment to using executive authority to fix what it perceives as flaws in the student loan system. This could mean:

- Further Simplification of PSLF: Efforts to streamline the PSLF application process and broaden the definition of qualifying employment or payments could continue, making it easier for public servants to achieve forgiveness.

- Enhanced IDR Benefits: The SAVE plan is already a significant step. By 2026, further adjustments could be made to IDR plans, such as reducing the percentage of discretionary income used for payments, increasing the poverty line exclusion, or even further shortening the repayment period for certain loan amounts.

- Targeted Forgiveness for Specific Groups: There may be continued focus on providing relief to specific groups, such as borrowers defrauded by predatory institutions, those with disabilities, or individuals in critical professions facing significant debt burdens.

This approach emphasizes administrative fixes and program improvements rather than broad, one-time forgiveness. It’s a more sustainable and legally less contentious path, but its impact is more incremental.

Scenario 2: New Legislative Action for Broader Forgiveness

A more impactful scenario for student loan forgiveness 2026 would involve legislative action. If Congress were to pass a bill authorizing widespread student loan forgiveness, it could provide relief to a much larger population of borrowers. However, this is politically challenging and depends heavily on the composition of Congress and the White House after upcoming elections.

- Potential for Capped Forgiveness: Any legislative forgiveness would likely come with income caps and a specific forgiveness amount (e.g., $10,000 or $20,000 per borrower).

- Focus on Undergraduate Debt: Legislation might prioritize forgiveness for undergraduate loans, or offer different tiers of forgiveness based on loan type or amount.

- Economic Stimulus Argument: Proponents would continue to argue that broad forgiveness acts as an economic stimulus, freeing up borrowers to spend, save, and invest more.

While this scenario offers the most significant potential for widespread relief, its feasibility is subject to the volatile nature of legislative politics.

Scenario 3: No Significant New Forgiveness, Focus on Repayment

It’s also possible that by 2026, there will be no significant new forgiveness initiatives. The focus might shift entirely to encouraging enrollment in existing IDR plans, improving loan servicing, and promoting financial literacy. This scenario would likely occur if:

- Political Stalemate: Legislative efforts fail, and the executive branch faces legal or political constraints on further unilateral action.

- Economic Recovery: If the economy is perceived to be strong, the urgency for broad debt relief might diminish.

- Budgetary Concerns: The long-term costs of forgiveness programs could become a more dominant concern, leading to a more conservative approach.

Even in this scenario, existing programs like PSLF and the SAVE plan would continue to provide pathways to forgiveness for eligible borrowers, but the prospect of new, broader relief under student loan forgiveness 2026 would be limited.

Who Stands to Benefit from Student Loan Forgiveness in 2026?

The impact of student loan forgiveness, whether through existing programs or new initiatives, is substantial. Over 40 million borrowers could be affected, though the extent of that impact varies greatly depending on the type and amount of forgiveness.

Targeted Relief Beneficiaries

Under the current trajectory of expanded existing programs, the primary beneficiaries for student loan forgiveness 2026 will continue to be:

- Public Servants: Teachers, nurses, social workers, government employees, and other non-profit workers who meet PSLF requirements stand to benefit significantly. The ongoing administrative changes aim to ensure that those who have dedicated their careers to public service receive the forgiveness they were promised.

- Low-Income Borrowers: The SAVE plan is particularly beneficial for borrowers with lower incomes, as it significantly reduces monthly payments and offers a faster path to forgiveness for smaller loan balances. This demographic will likely see the most immediate and substantial relief through IDR plans by 2026.

- Long-Term Borrowers: Individuals who have been faithfully making payments for 20-25 years (or even 10 years under SAVE for smaller balances) under IDR plans will continue to see their remaining balances forgiven. Recent adjustments have retroactively counted more payment periods towards forgiveness, accelerating this process for many.

- Defrauded Students: Victims of predatory for-profit institutions will likely continue to receive targeted discharge of their loans.

Potential Broader Beneficiaries

Should legislative action for broader forgiveness materialize by student loan forgiveness 2026, the pool of beneficiaries would expand dramatically. This could include:

- Middle-Income Borrowers: Those who may not qualify for PSLF or whose incomes are too high for significant IDR benefits might receive a lump sum of forgiveness.

- Recent Graduates: A fresh start for those just entering the workforce, potentially easing the financial burden as they begin their careers.

- Borrowers with Smaller Balances: Even a modest amount of forgiveness could completely eliminate debt for millions of borrowers with smaller outstanding balances, providing immediate relief.

The key takeaway is that while the specifics of student loan forgiveness 2026 are still being shaped, a significant portion of the 40 million borrowers will likely find some form of relief available to them, whether through enhanced existing programs or new initiatives.

Navigating Your Options: Preparing for Student Loan Forgiveness in 2026

Regardless of the political winds, borrowers can take proactive steps now to position themselves for any potential student loan forgiveness 2026 opportunities or to optimize their current repayment strategies.

1. Understand Your Loan Types

Not all student loans are created equal when it comes to forgiveness. Federal student loans (Direct Loans) are generally eligible for the widest range of forgiveness programs. Private student loans are almost never eligible for federal forgiveness programs. Consolidating older federal loans (like FFEL or Perkins Loans) into a Direct Consolidation Loan can sometimes make them eligible for PSLF and certain IDR benefits.

2. Enroll in an Income-Driven Repayment (IDR) Plan

If you haven’t already, explore and enroll in an IDR plan, especially the new SAVE plan. IDR plans are the most common pathway to forgiveness for federal loans, outside of PSLF. Your monthly payments are based on your income and family size, and any remaining balance is forgiven after a certain number of years. Even if you don’t anticipate forgiveness, lower payments can ease your financial burden. For many, this is the most direct path to student loan forgiveness 2026 or soon after.

3. Check PSLF Eligibility and Certify Employment

If you work for a government agency (federal, state, local, or tribal) or a qualifying non-profit organization, investigate PSLF. The program has been significantly reformed to be more accessible. Make sure to certify your employment annually, even if you haven’t been making payments, to track your progress towards the 120 qualifying payments. Don’t wait until 2026 to start this process.

4. Keep Your Contact Information Updated

Ensure your loan servicer and the Department of Education have your most current contact information. Important updates about forgiveness programs, eligibility changes, and application deadlines will be communicated through these channels. Missing critical information could mean missing out on student loan forgiveness 2026.

5. Be Wary of Scams

The promise of student loan forgiveness often attracts scammers. Be extremely cautious of any company or individual that asks for upfront fees to help you with forgiveness, guarantees immediate forgiveness, or asks for your FSA ID password. Official communications will come directly from your loan servicer or the Department of Education, and there are no fees for federal forgiveness applications.

6. Stay Informed and Advocate

The student loan landscape is dynamic. Follow reputable news sources, government announcements, and non-profit organizations focused on student debt. Consider joining advocacy groups if you feel strongly about broader forgiveness measures. Your voice, combined with others, can influence future policy decisions regarding student loan forgiveness 2026 and beyond.

The Broader Economic and Social Implications

The discussion around student loan forgiveness 2026 is not merely about individual relief; it has profound economic and social implications. The sheer scale of student debt in the U.S. ($1.7 trillion) means that any significant policy change reverberates throughout the economy.

Economic Impact

- Consumer Spending: Forgiven debt can free up disposable income, potentially leading to increased consumer spending, which can stimulate economic growth.

- Housing Market: Student debt is often cited as a barrier to homeownership, particularly for younger generations. Forgiveness could enable more individuals to save for down payments and enter the housing market.

- Entrepreneurship: Reduced debt burdens might encourage more individuals to take entrepreneurial risks, fostering innovation and job creation.

- Inflation Concerns: Critics often raise concerns that widespread forgiveness could contribute to inflation by injecting more money into the economy. This is a key point of debate in any legislative discussion about student loan forgiveness 2026.

Social Impact

- Equity and Opportunity: Student debt disproportionately affects minority borrowers and those from lower socioeconomic backgrounds. Forgiveness can be seen as a tool to address historical inequities and promote greater social mobility.

- Mental Health: The stress associated with significant debt can have serious mental health consequences. Relief from this burden can improve overall well-being for millions.

- Educational Attainment: Some argue that the promise of forgiveness could encourage more individuals to pursue higher education, potentially leading to a more educated workforce. Others worry it could incentivize over-borrowing.

The debates surrounding these impacts will continue to shape the policy decisions that ultimately determine the scope and nature of student loan forgiveness 2026.

Conclusion: A Path Forward for Borrowers

The prospect of student loan forgiveness 2026 remains a complex and evolving topic. While widespread, one-time forgiveness faces significant political and legal hurdles, the trend towards targeted relief and more accessible pathways through existing programs is clear. The SAVE plan, in particular, represents a substantial step forward in making federal student loan repayment more manageable and offering a clear path to forgiveness for many.

For the millions of borrowers impacted, the best strategy is to stay informed, understand your specific loan types, and proactively engage with available federal programs. Don’t wait for a broad forgiveness announcement; instead, optimize your current repayment strategy by enrolling in IDR plans, certifying PSLF employment if applicable, and keeping your information up-to-date. By taking these steps, you empower yourself to navigate the student loan landscape effectively and maximize your chances of benefiting from any form of student loan forgiveness 2026 or beyond.

The conversation around student loan debt and its forgiveness will undoubtedly continue to be a central theme in national policy discussions. For borrowers, remaining educated and engaged is the most powerful tool in securing a more stable financial future.