IRS Tax Code Changes 2026: Key Deductions & Credits for Small Businesses

The landscape of taxation is in perpetual motion, and for small businesses, staying abreast of these shifts is not merely advisable but absolutely critical for financial health and sustained growth. As we look towards 2026, the Internal Revenue Service (IRS) is poised to implement a series of tax code changes that could profoundly impact how small enterprises operate, plan, and ultimately, pay their taxes. This comprehensive guide is designed to dissect these impending IRS Tax Changes 2026, offering an in-depth analysis of key deductions, credits, and strategic considerations that every small business owner must understand.

Understanding the nuances of these changes early allows for proactive planning, which can translate into significant savings and prevent costly compliance issues. From potential modifications to the Qualified Business Income (QBI) deduction to shifts in depreciation rules and new opportunities for tax credits, the forthcoming tax year promises both challenges and opportunities. Our aim is to provide you with a clear roadmap to navigate this evolving tax environment, ensuring your business is not just compliant, but optimally positioned for success.

The Looming Specter of IRS Tax Changes 2026: A General Overview

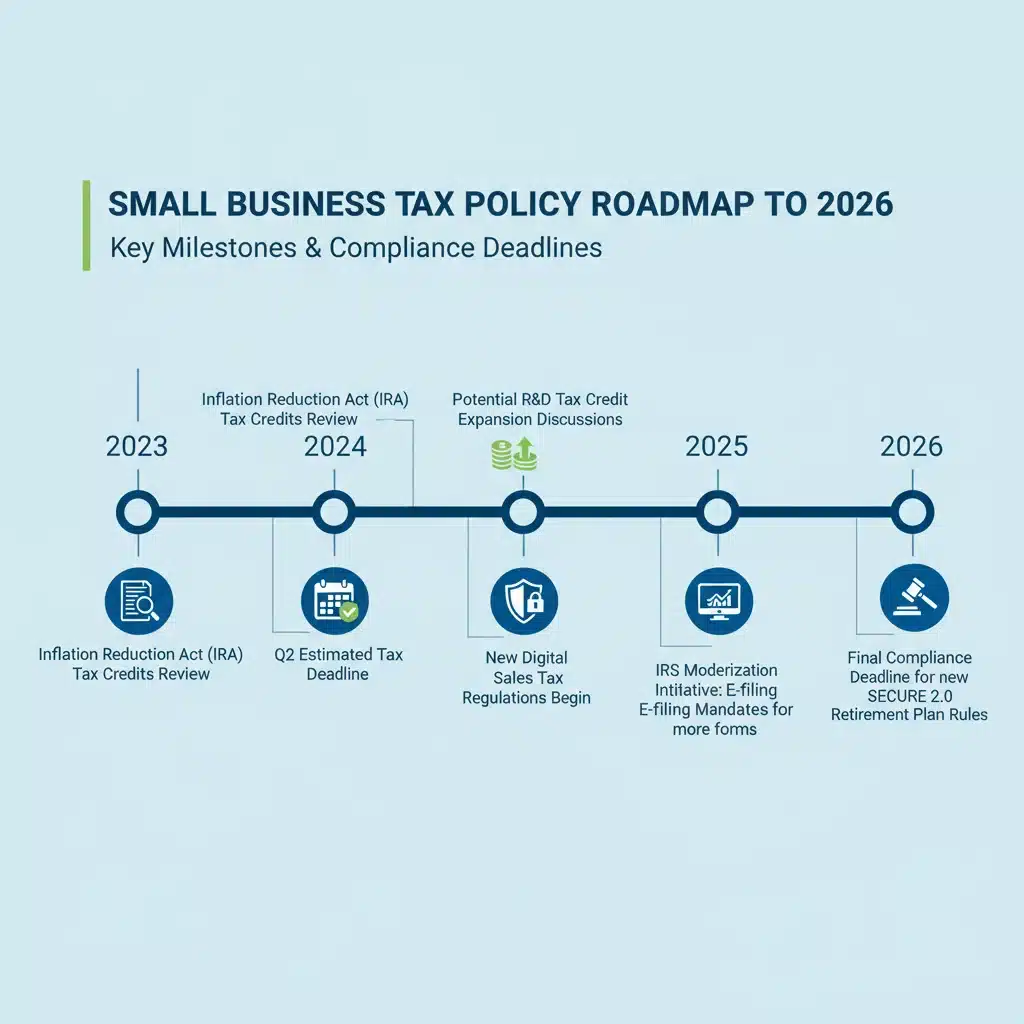

The year 2026 is significant because many provisions from the Tax Cuts and Jobs Act (TCJA) of 2017 are set to expire or undergo significant modification. While some aspects may become permanent, others are scheduled to revert to pre-TCJA rules, or new legislation might introduce entirely fresh frameworks. For small businesses, this creates a dynamic and somewhat uncertain fiscal future. The potential for substantial alterations to individual and corporate tax rates, as well as specific business deductions, demands careful attention.

One of the most talked-about elements is the potential sunsetting of individual income tax rate reductions. While small businesses often operate as pass-through entities (sole proprietorships, partnerships, S corporations), meaning their income is taxed at the owner’s individual rates, any change to these rates directly impacts their effective tax burden. Beyond individual rates, there’s also the possibility of adjustments to the corporate tax rate, which could affect C-corporations. Furthermore, the political climate leading up to 2026 will heavily influence the final shape of these tax laws, making it imperative for business owners to remain informed and adaptable.

Key Deductions on the Chopping Block: What Small Businesses Need to Know

Several critical deductions that small businesses have relied on might see significant changes or even expiration in 2026. Proactive planning is essential to mitigate any adverse effects.

Qualified Business Income (QBI) Deduction (Section 199A)

Perhaps the most impactful change for many pass-through entities is the potential expiration of the Section 199A QBI deduction. Introduced by the TCJA, this deduction allows eligible self-employed individuals and owners of pass-through businesses to deduct up to 20% of their qualified business income, subject to various limitations. Its potential expiration would mean a significant increase in taxable income for many small business owners.

- Impact: If the QBI deduction expires, businesses currently benefiting from it will see their taxable income rise, leading to a higher tax liability.

- Strategy: Businesses should model their finances with and without the QBI deduction to understand the potential impact. Consider accelerating income or deferring expenses if it aligns with your overall tax strategy, but consult with a tax professional.

Bonus Depreciation and Section 179 Expensing

The TCJA also enhanced bonus depreciation, allowing businesses to immediately deduct 100% of the cost of eligible new and used property placed in service. This rate began to phase down in 2023 and is scheduled to continue declining, reaching 0% by 2027. Similarly, Section 179 expensing allows businesses to deduct the full purchase price of qualifying equipment and/or software purchased or financed during the tax year, up to certain limits. While Section 179 is permanent, its limits and phase-out thresholds are subject to annual adjustments and potential legislative changes.

- Impact: The reduction in bonus depreciation will mean businesses will have to depreciate assets over longer periods, delaying tax savings. Changes to Section 179 limits could also affect immediate write-offs.

- Strategy: Businesses planning significant capital expenditures should consider accelerating these purchases to take advantage of higher bonus depreciation rates while they last. Regularly review Section 179 limits to maximize immediate deductions.

Business Interest Expense Limitation (Section 163(j))

The TCJA introduced a limitation on the deduction for business interest expense, generally capping it at 30% of adjusted taxable income (ATI). For tax years beginning in 2022, the definition of ATI became more restrictive, no longer allowing the add-back of depreciation, amortization, and depletion. This makes the limitation more impactful for many businesses. While not set to expire, its calculation could be further refined by future legislation.

- Impact: Businesses with significant debt or those undergoing substantial capital investments might find their interest deductions limited, increasing taxable income.

- Strategy: Monitor your interest expense relative to your ATI. Consider debt restructuring or alternative financing options if the limitation significantly impacts your tax position.

Emerging and Evolving Tax Credits: Opportunities for Small Business Growth

While some deductions may be curtailed, new or enhanced tax credits could offer valuable offsets to tax liabilities. Small businesses should explore these opportunities diligently.

Research and Development (R&D) Tax Credit

The R&D tax credit remains a powerful incentive for businesses investing in innovation. While the TCJA mandated that R&D expenses must be capitalized and amortized over five years (or 15 years for foreign R&D) starting in 2022, there is ongoing bipartisan support to reverse this change and restore immediate expensing. Future legislation in 2026 could address this, making the credit even more attractive.

- Impact: The current capitalization requirement delays the tax benefit. A potential reversal would significantly improve cash flow for innovative businesses.

- Strategy: Continue to track all eligible R&D expenses. Stay informed about legislative efforts to restore immediate expensing, as this could significantly impact your accounting and tax planning.

Clean Energy and Energy Efficiency Credits

The Inflation Reduction Act (IRA) of 2022 introduced or expanded numerous clean energy and energy efficiency tax credits, many of which extend well beyond 2026. These credits can benefit small businesses investing in renewable energy systems (solar, wind), energy-efficient equipment, or clean vehicles.

- Impact: Significant tax savings for businesses adopting sustainable practices and technologies.

- Strategy: Evaluate your energy consumption and equipment. Explore opportunities to invest in eligible clean energy solutions or upgrade to energy-efficient alternatives. Many of these credits have direct pay or transferability options, further enhancing their value.

Employee Retention Credit (ERC) Aftermath

While the Employee Retention Credit (ERC) was a temporary pandemic-era relief measure, its impact and the ongoing IRS scrutiny of fraudulent claims continue to be relevant. Small businesses that claimed the ERC should be prepared for potential audits and understand the compliance requirements, even as new credits might emerge.

- Impact: Potential for audits and penalties for improperly claimed ERC.

- Strategy: Ensure all ERC claims are thoroughly documented and justifiable. If you have concerns, consult with a tax professional experienced in ERC compliance.

Strategic Tax Planning for IRS Tax Changes 2026

Given the potential for significant IRS Tax Changes 2026, a proactive and dynamic tax planning strategy is paramount. Waiting until the end of the year to assess your tax situation could lead to missed opportunities or unexpected liabilities.

Regular Financial Health Checks

Consistent monitoring of your business’s financial performance is the foundation of effective tax planning. Understand your revenue streams, expense categories, and profit margins. This data will be crucial for modeling different tax scenarios.

- Action: Implement robust accounting practices. Use financial software to generate regular reports and track key performance indicators.

Scenario Planning and Modeling

Work with your tax advisor to develop various tax scenarios based on potential legislative outcomes. What if the QBI deduction expires? What if bonus depreciation is further reduced? Modeling these possibilities allows you to understand the potential impact on your cash flow and profitability.

- Action: Create ‘best-case,’ ‘worst-case,’ and ‘most-likely’ tax scenarios for 2026. This will help you identify potential vulnerabilities and opportunities.

Capital Expenditure Review

If your business anticipates large purchases of equipment, vehicles, or property, the timing of these investments could significantly affect your tax liability. With bonus depreciation phasing out, accelerating purchases into earlier tax years might be advantageous.

- Action: Review your capital expenditure budget for the next few years. Consult with your tax advisor on optimal timing for these investments to maximize depreciation benefits.

Income and Expense Timing

For cash-basis taxpayers, the timing of income recognition and expense payments can be a powerful tax planning tool. Consider accelerating deductions into higher-tax years or deferring income into lower-tax years, depending on the anticipated tax rate changes.

- Action: Discuss income and expense deferral/acceleration strategies with your tax professional, especially as 2026 approaches.

Reviewing Business Structure

The optimal business structure (sole proprietorship, partnership, S-corp, C-corp) can significantly influence your tax burden, especially with changes to individual and corporate rates. While changing your business structure is a complex decision with legal and operational implications, 2026 might be a good time to re-evaluate if your current structure remains the most tax-efficient.

- Action: Consult with both a tax advisor and a legal professional to assess if your current business structure is still optimal given the projected 2026 tax environment.

Staying Compliant Amidst the Changes

Compliance is non-negotiable. As tax laws evolve, so do the requirements for accurate record-keeping and reporting. The IRS continues to enhance its enforcement capabilities, making meticulous compliance more important than ever.

Enhanced Record-Keeping

The complexity of new tax laws often comes with increased demands for detailed documentation. Ensure your record-keeping systems are robust enough to support all deductions and credits claimed.

- Action: Invest in reliable accounting software. Digitize receipts and financial records. Maintain clear documentation for all business expenses, investments, and transactions.

Understanding New Forms and Reporting Requirements

New tax laws frequently introduce new forms or modify existing ones. Familiarize yourself with these changes to avoid errors and delays in filing.

- Action: Stay updated with IRS publications and announcements. Work closely with your tax preparer to ensure all necessary forms are completed accurately.

Leveraging Professional Expertise

Navigating complex tax changes is challenging, even for seasoned business owners. A qualified tax professional can provide invaluable guidance, ensuring compliance and identifying opportunities for tax optimization.

- Action: Establish a strong relationship with a Certified Public Accountant (CPA) or an enrolled agent specializing in small business taxation. Schedule regular meetings to discuss your financial situation and plan for upcoming tax years.

The Broader Economic and Political Context

It’s important to remember that tax policy doesn’t exist in a vacuum. The IRS Tax Changes 2026 will be shaped by the prevailing economic conditions and the political landscape. Factors such as inflation, economic growth rates, and the outcome of elections will all play a role in how tax legislation is ultimately crafted and implemented.

Inflation and Tax Brackets

While tax brackets are typically adjusted for inflation annually, significant inflationary pressures can erode the real value of deductions and credits if they are not similarly indexed or if the adjustments lag behind. Small businesses need to consider how inflation impacts their costs, revenues, and ultimately, their taxable income.

Potential for Further Legislative Action

The period leading up to and including 2026 could see additional legislative efforts beyond merely addressing the TCJA sunsets. Policymakers may introduce new tax incentives for specific industries, address social or environmental concerns through tax policy, or seek to reform the tax system more broadly. Staying informed about these potential developments is crucial.

Impact on Business Investment and Growth

Tax policy plays a significant role in incentivizing or disincentivizing business investment, hiring, and overall growth. Changes to depreciation rules, capital gains taxes, or tax rates can influence business decisions regarding expansion, research, and development. Small businesses should consider how these changes might affect their long-term strategic plans.

Preparing for the Future: A Continuous Process

Tax planning is not a one-time event but an ongoing process. As 2026 draws nearer, the clarity around specific tax changes will improve, but the need for continuous vigilance and adaptation will remain.

Engage with Industry Associations

Many industry associations actively lobby for their members’ interests in tax policy debates. Being an active member can provide you with early insights into proposed changes and opportunities to voice your concerns.

Utilize IRS Resources

The IRS website is a primary source for official guidance, forms, and publications. Regularly check for updates and subscribe to IRS news releases relevant to small businesses.

Internal Review and Training

Ensure your internal accounting team or staff responsible for financial management are educated on the impending changes. Regular training and updates can prevent costly errors.

Conclusion: Navigating the IRS Tax Changes 2026 with Confidence

The upcoming IRS Tax Changes 2026 present a complex but navigable landscape for small businesses. While the potential expiration of key deductions and the introduction of new credits might seem daunting, a proactive approach to understanding and planning for these changes can turn potential challenges into strategic advantages. By staying informed, engaging in meticulous record-keeping, conducting thorough scenario planning, and leveraging the expertise of tax professionals, small business owners can ensure they are well-prepared to meet the demands of the evolving tax code.

The goal is not just to comply but to optimize. By strategically adapting to the new rules, small businesses can minimize their tax burden, preserve capital, and continue to invest in their growth and future success. Start your planning today, and position your business to thrive in the post-2026 tax environment.